According to this article, “high growth of the telecommunication industry and increased prominence of the environment-friendly trenchless technology are expected to drive demand” and will help continue the growth of the industry as a whole from its estimated market size of USD 5.12 billion in 2014.

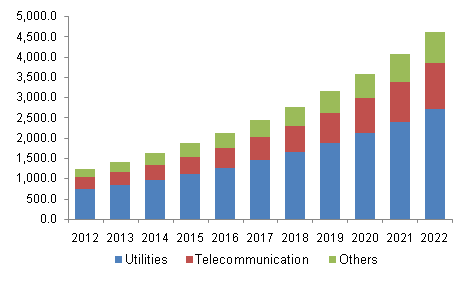

North America horizontal directional drilling marketing by end-use, 2012-2022, (USD Million)

With the many industries that tie-in to Underground Boring seeing growth as well (natural gas, power companies, telecommunication) it’s a good time to be thinking about your long-term strategy. Is your equipment up to the task of assisting all of these potential customers through this period of expansion? If not, how are you going to pay for it? “We have enough cash”. While that may be true, we’ve found that paying cash for equipment can actually be a drain to your business. Finding a good lending partner can help you acquire equipment using monthly payments, so you can free up your funds for other growth-oriented endeavors. SLS is a great option for used equipment, and we would be happy to help! In other circumstances, here are a few good options and the qualities of a good lending partner for your needs.

How to Find a Good Lending Partner for Underground Boring / Horizontal Directional Drilling

![]()

Manufacturers: Manufacturers, like Ditch Witch, often offer financing themselves, and can be your best option in a lot of cases. Check the website of the manufacturer you’re working with to see if they offer financing for their equipment.

![]()

Your local bank is usually a good choice, however, given that they may not be familiar with underground boring equipment, this may not be the path of least resistance. So ~ as you begin your search (under most normal circumstances) you should do the following things to determine if you are working with a quality equipment leasing / financing professional – see below:

Upfront Monies: If a lender asks for money upfront ~ you’re up the wrong money tree! Once you are APPROVED & receive documentation, then & only then should you send the lender any needed down payment or advance payment along with your signing of a credit-approved final contract.

Furthermore, check for the following ~

Reputation: That the commercial lender has a great reputation. But, how do you know? Easy enough ~ Google the company name and the city and state. You are just looking for complaints. Be careful if you see many (more than a couple) of these! If so, choose another.

Longevity: Has this company been around for 10 or 20 years or more? A seasoned organization, with no complaints is often a great way to go.

The Contract: Review the contract and verify that these are the final terms & that you are indeed credit approved. Verify too that they are ready to fund once you send in the final contract. If this is not the case … you’re better off with someone else.

Once you find a credible lender it is time for underwriting.

Get a financing or equipment leasing quote and complete a credit application.

Many well-established lenders offer an online application ~ like this:

Online Application: Click Here

Terms and Payments for underground boring equipment can vary based on the amount of money involved and your overall credit profile.

Also ~ whether the equipment is new or used can sometimes impact the terms available for borrowers.

Payment Example ~

Underground boring equipment cost ~ $100,000 & a 5 year term –

- Monthly payments will usually range from $2000 – $2500 (subject to credit approval, of course.)

Many National Commercial Lenders offer A, B and C Options and thus the differences. Financing terms are typically from 2 – 5 years. Here are some factors that aid them in underwriting a company’s credit application:

Time in business: The newer the company the greater the monthly payment.

Personal Credit Score: The lower the credit score the greater the monthly payment ~ all things being equal.

Many other factors help a lender to analyze the risk associated with a underground boring professional applicant.

Usually the 5 C’s of Credit come into play when a lender analyzes an applicant.

Character / Credit: Personal and business credit scores and the like help the lender understand this C as it relates to an applicant.

Capacity: Show me the money! Capacity to pay is all about cash flow. Many underground boring equipment lenders ask for a copy of 3 recent bank statements. These are easy to obtain & forward thanks to online banking. This shows how much you are making & spending in each of the months presented.

Collateral: What is the equipment worth now and what will it be worth in the future? This helps to show a creditor the value of the collateral.

Conditions: Right now, conditions for the underground boring industry are positive. Your industry follows the economy to a great extent. Building is surging, as is the economy in general, so this is great time to be in your industry.

Capital: How much money or wealth do you have in your company?

Sound complicated? It doesn’t have to be! We have over 30 years of experience at SLS Financial Services helping people just like you finance new and used equipment so that you can focus on growing your business. If you’re ready to add the benefits of new equipment to your ever-growing business, we’re ready to help you make the process… Uncomplicated! We aren’t your typical commercial lender. We look at the person behind the application. If you have any questions about our process feel free to reach out to us at 816-587-3400 or you can find a link to our application below.

Today, credit scoring systems can make credit decisions almost instantly. However, business is still about people. More than ever, business-owners seek (a) commercial lending partner to learn about their unique needs and be solution-providers.

Speed and technology are important, but do they come at the expense of leaving people, their story, and opportunities behind?

At SLS, we’ve never lost focus on the business-owner behind the application. A big part of our success is based on customer satisfaction ~ plain & simple, because we believe in leveraging technology and combining it with our expertise for only one purpose…to help people.

Call Doug for more information ~ 816.863.3070

President of SLS Financial, an accountant, former Board Member of one of the safest banks in America, and owner of multiple businesses.

For more than 30 years he has assisted buyers and sellers of equipment with competitive finance and commercial lending programs.

Contact Doug:

816.423.8021

Recent Comments